Investors are seeing a lot of first-time-in-history, worst-on-record data points in this Covid induced economic lockdown. And we just saw another milestone, this time in crude oil.

Headlines would have you believe that the price of oil turned negative last night. But it’s not quite the apocalyptic scenario this would imply.

The US benchmark for crude oil, West Texas Intermediate (WTI), plummeted 300% in a single day, from $18 a barrel to minus $37.45. It was the first time in history that the index settled below zero. The speed of the drop was also shockingly fast.

Stock markets in Europe reacted negatively to the slew of news reports, opening sharply lower on the morning of 21 April.

But if oil really was selling for less than $0, we would see a similar move in the other major index, Brent crude, which is the international benchmark used by OPEC countries like Saudi Arabia and Kuwait.

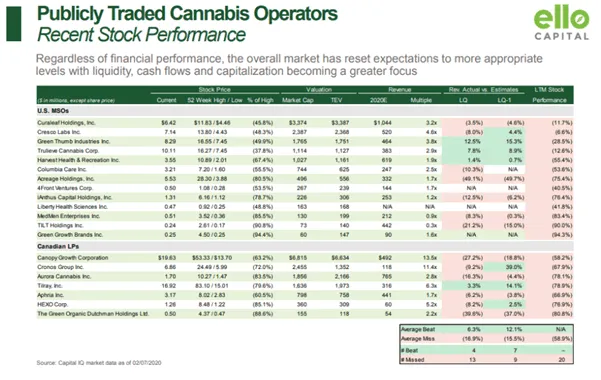

If we look at the oil price table from late on 20 April 2020, that’s clearly not the case.

Still, I’ve never seen the WTI trading negative before. No one has. So what really happened?

Source: Oilprice.com

A technical oddity

The largest futures market on the planet, the CME, confirmed to its members last night that oil futures “have no low limit and can trade negative”. This was news to most, who have never seen oil futures trade below zero before.

Analysts like Tom Kloza, the head of global markets for the Oil Price Information Service, were left stunned. He told Marketwatch:

“I’m not sure how to react to this other than to say that nobody has ever seen oil prices this low before.”

But we need to separate crude oil futures from the price of the underlying asset.

And the power of huge oil ETFs is particularly important.

What really happened

The steep drop into negative prices was brought about not just by the glut of overproduction and storage venues nearing their limits. It is also a matter of timing.

The May futures contract for crude oil expired on Monday 20 April.

In futures markets, participants are traders gambling on the future price of the black liquid. If they think the price of oil is going to rise, they will buy a futures contract and in theory will be able to sell that contract for a profit down the line. Buyers and sellers set the price, and trade contracts back and forth many times a day.

ETFs for crude oil allow investors to get exposure to the price of oil without getting their hands dirty and actually going onto markets to buy and sell commodities. And ETFs are hugely powerful. As the May futures contract deadline approached the United States Oil Fund (NYSEARCA:USO) held more than 28% of the outstanding shares.

Under the strict terms of these futures contracts, when they end, holders have an obligation to take delivery of 1,000 barrels of crude oil for every contract they own at the time. These would be delivered to the main American storage hub in Oklahoma, and traders left holding these contracts would have to pay to store them.

Clearly an ETF does not actually want to take delivery of thousands upon thousands of barrels of crude, nor have to pay to store it in a warehouse.

The futures market works on simple supply and demand. When there are lots of sellers and no buyers wanting to take on worthless options, the price dives. It did so spectacularly on Monday as mass panic set in, and sellers like the ETF started dumping these contracts onto futures markets at any price.

With no buyers in sight and only hours until the time limit rolled around, the price for the contract plummeted to its historic low.

Where oil is now

The proof that the massive buying power of ETFs was the source of this precipitous plunge is in looking at the price of contracts that will expire in June, July, August and beyond.

June’s contract is sharply down, but is trading at $18.95 a barrel. That contract starts on Tuesday 21 April and ends on Tuesday 19 May. July 2020’s contract is at $24, August at $26, September at $28 and so on. The further away we get from the coronavirus crisis, the more the market thinks the price of oil will rise.

So this event does speak to the underlying weakness in fragile markets, but it’s not an oil apocalypse.

In truth, negative oil futures was a one-off event. An unprecedented one-off event, sure, but a technical oddity all the same.