Social media powerhouse Facebook (NASDAQ: FB) reports its FY21 Q2 Earnings on Wednesday, July 28.

Facebook beat analyst estimates in its Q1 earnings to the end of March 31. Continuing this trend, analyst consensus estimates predict continued revenue growth in Q2.

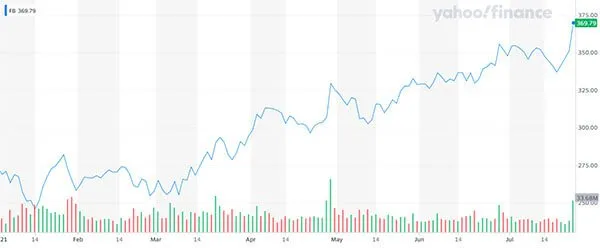

#Facebook share price overview

The Facebook share price has risen over 198% in the past five years. It is up 58% in the past year and 21% in the past three months.

Despite some negative headlines and rumors of a mass exit from the social media goliath, Facebook remains a popular stock.

Facebook share price chart year-to-date – Source: Yahoo Finance

According to Koyfin data, the 12-month average share price target is $388. This gives a 5% upside from here. The majority of brokers mark FB stock a Buy.

As of July 23. Facebook financial metrics come in as follows:

Share Price: $369.79

Market Cap: $1.04 Trillion

Trailing 12-Month (TTM) Revenue: $94.4bn

TTM Cash and Short Term Investments: $64.22bn

Total Assets: $77.3bn

Debt: $12.14bn

Total Equity: $133.65bn

TTM EPS: 11.67

TTM P/E Ratio: 31.48

#Q2 Predictions

Investors will be looking to see if it can retain its advertising revenue growth. Analyst consensus believes it will.

Q1 advertising revenue grew 30% year-over-year.

In its Q1 earnings call, Facebook indicated it expects advertising revenue growth to continue sideways or upwards through Q2. However, it also noted Apple’s latest restrictions might cause headwinds.

Apple is giving users more privacy control, which could lead Facebook to receive less data. The data Facebook takes from Apple is used to profile users and target them with ads.

Consensus EPS forecasts for Q2 come in at $3.02, a rise of 67% year-over-year. At the same time, revenue is expected to come in at $27.82bn, up 60% year-over-year.

#Shareholder risks:

Competition is rising, and Apple’s move to further protect user privacy is causing an ongoing headache for Facebook.

There are also rumors swirling that many influencers and significant users have jumped ship to competing platforms. With Snapchat (N: SNAP), Twitter (NYSE: ), TikTok, YouTube, Discord, and Telegram all offering new and unique ways to reach audiences, consumers have no shortage of choice.

Facebook is no stranger to regulatory scrutiny and has faced mounting pressure the bigger it gets. However, a recent milestone case was thrown out of court, leaving Facebook momentarily celebrating.

This is far from over, however. Due to its part to play in spreading fake news and harmful content, there are plenty of politicians and significant forces with a bone to pick with Facebook.

These are all points investors should bear in mind before buying shares.

#Why bullish sentiment abounds

With access to stacks of cash, Facebook is in the enviable position of being able to fight its battles with a competitive edge.

CEO Mark Zuckerberg has already committed to making the platform small-business friendly. He’s also planning on improving its ability to give creatives a lucrative and user-friendly space to dominate while making a living.

This is not just for Etsy (NASDAQ: ETSY) style cottage industry crafts but also for streamers, influencers, writers, podcasters, and gaming creators.

Facebook is quite happy to watch out for money-spinning hits and adopt them as its own. It’s also moving into augmented reality (AR) and virtual reality, which some believe will be a future game-changer for the firm.

Its vision is for Facebook to become a metaverse, where users are completely immersed in the virtual environment. A place where they work, game, and socialize using VR headsets.

Facebook has tremendous access to user data, consumer insights, and cash at its disposal, so it can afford to fail in its quest for greatness. However, it comes with several pitfalls and investors need to go in with eyes open.